Risk Management

Geopolitical Tail Risk Manager

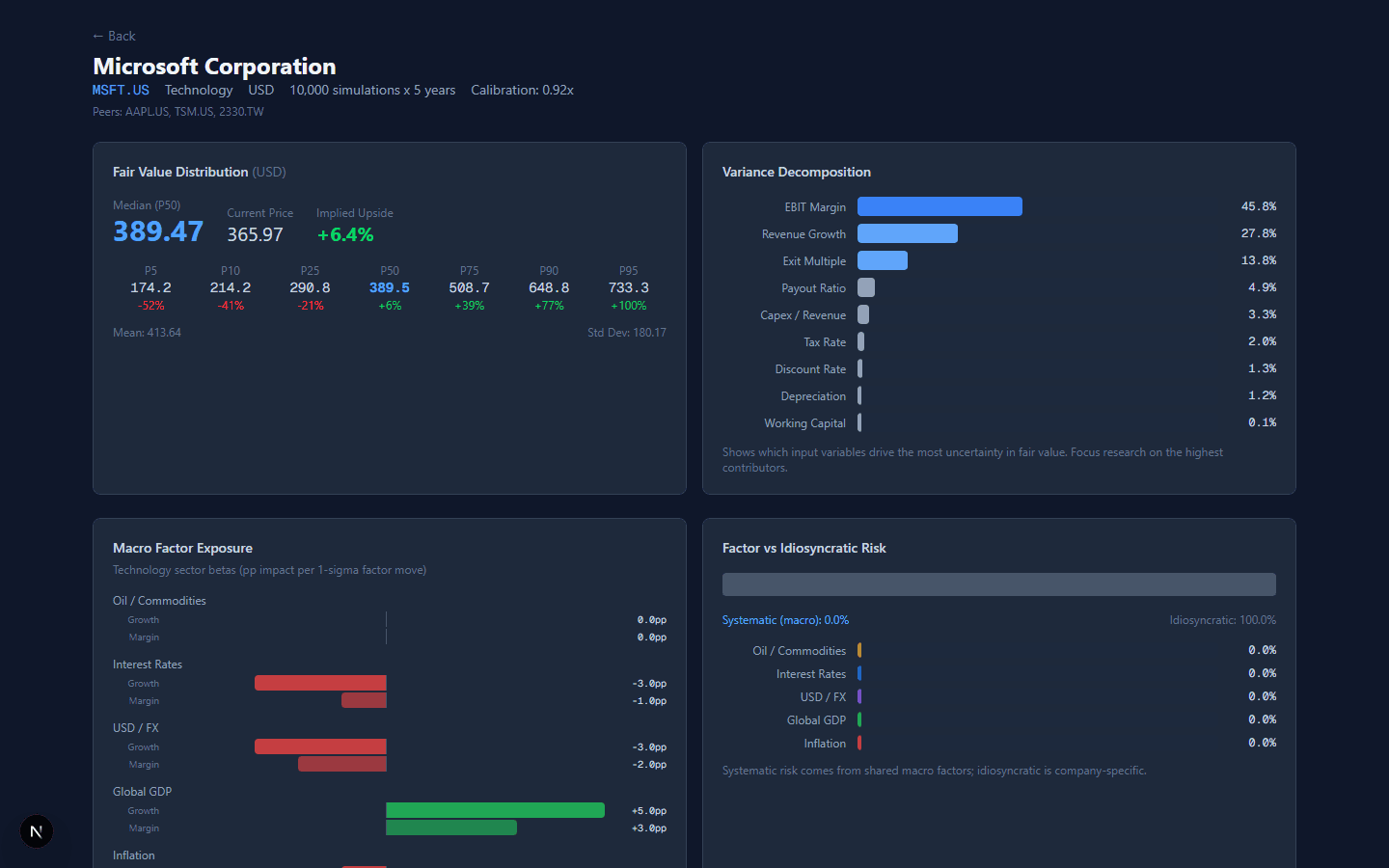

Risk scenario modelling for mapping geopolitical events to portfolio exposures. Probability-weighted impact analysis with tail distribution visualisation and Monte Carlo simulation across multiple risk scenarios.

Next.jsFastAPID3.jsPython